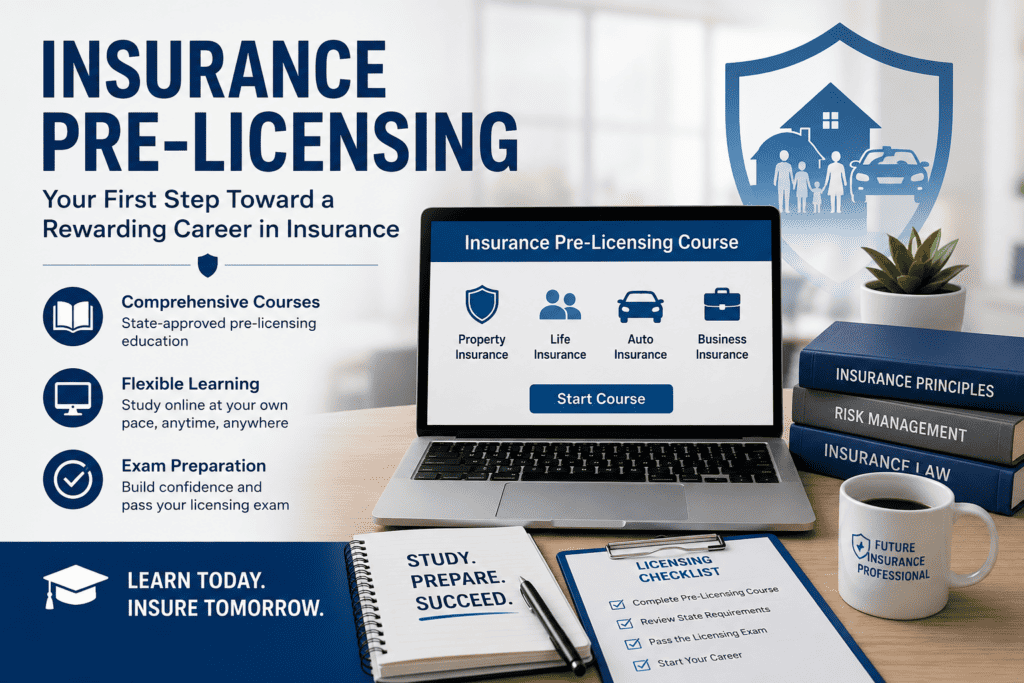

The California Department of Insurance (CDI) has introduced a new 8-hour annuity training requirement aimed at enhancing consumer protection and ensuring insurance professionals are well-versed in the intricacies of annuity products. California’s new 8-Hour Annuity Training updates the state’s commitment to equipping insurance agents with the knowledge necessary to offer suitable recommendations and maintain transparency.

Here’s what insurance professionals need to know about this important update.

Complete the new CA 8-Hour Annuity Training course today

Background: Why the Change?

Annuities are complex financial products that serve as an essential tool for retirement planning. However, their intricacies often make it challenging for consumers to fully understand their benefits, costs, and risks. CDI’s updated training standard aligns with the National Association of Insurance Commissioners (NAIC) Model Regulation #275, which seeks to ensure that consumers receive clear and informed guidance.

This change is designed to:

- Protect consumers by improving the quality of recommendations.

- Ensure compliance with California’s best interest standards.

- Provide agents with comprehensive knowledge of annuity types, benefits, and risks.

The Key Requirements

- Initial Training for New Agents

All newly licensed agents who intend to sell annuity products in California must complete 8 hours of training before offering or soliciting annuities. This foundational course covers critical topics, including:- Types and classifications of annuities.

- Suitability and best interest standards.

- Tax implications and benefits of annuities.

- How to address potential consumer concerns.

- Ongoing Training for Existing Agents

Agents who have already completed their initial annuity training must complete a 4-hour refresher course every two years to stay current on regulatory updates and emerging trends. - Focus on Best Interest Standards

A significant portion of the training focuses on the best interest obligations outlined in recent regulations. Agents are required to prioritize consumer needs over their own compensation and ensure recommendations align with the client’s financial goals.

How This Impacts Insurance Professionals

The new requirements might feel like an additional step, but they offer long-term benefits:

- Enhanced Credibility: Comprehensive training builds trust with clients, as it ensures agents can clearly explain the nuances of annuity products.

- Compliance Assurance: Staying updated with regulatory standards minimizes the risk of legal and financial penalties.

- Competitive Advantage: Agents who demonstrate a deeper understanding of annuity products are more likely to gain a competitive edge in the marketplace.

Conclusion

The new 8-hour annuity training requirement reflects California’s dedication to protecting consumers while ensuring agents are well-equipped to navigate the complexities of annuity sales. While it may require additional time and effort, this update is an opportunity for insurance professionals to enhance their skills, build trust with clients, and ensure compliance in a competitive industry.

By embracing these changes proactively, agents can not only meet regulatory obligations but also position themselves as knowledgeable and trustworthy advisors in the evolving insurance landscape.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

Need Continuing Education? Create an Account to Start Today