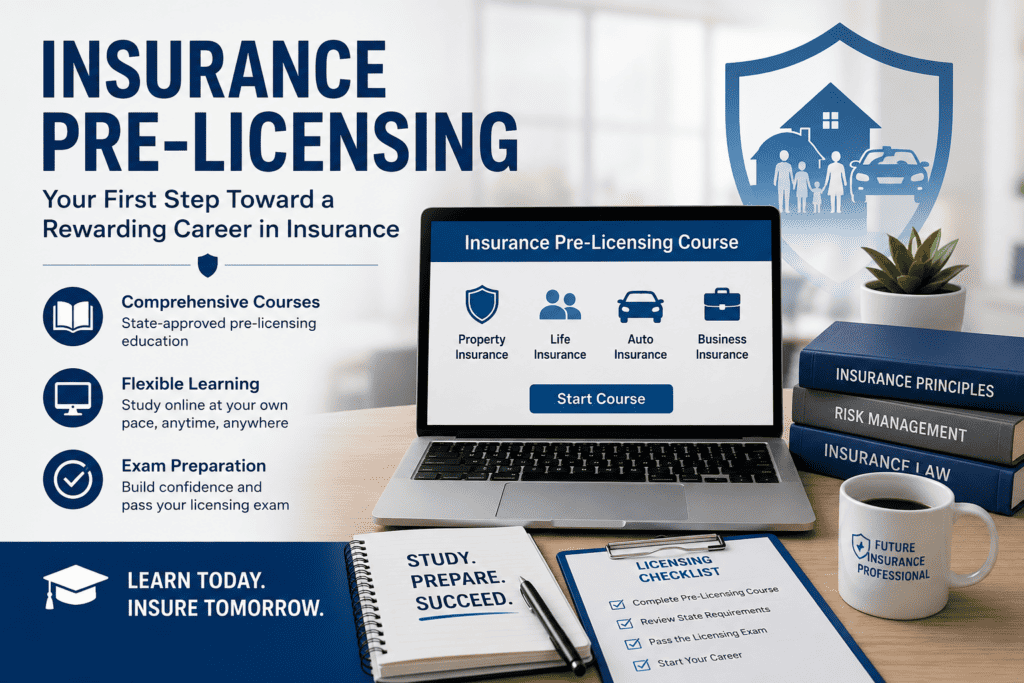

Success CE is pleased to announce that, effective June 1, 2026, our insurance pre-licensing courses are now available in all 50 states effective June 1, 2026

This nationwide expansion allows aspiring insurance professionals across the country to access the training and educational resources needed to prepare for their state licensing examinations and launch successful careers in the insurance industry.

We provide comprehensive, easy-to-understand instruction designed to help students build knowledge, confidence, and exam readiness.

For information regarding available courses, state-specific licensing requirements, and enrollment options, please visit our website or contact our team directly.

As the insurance industry continues to grow and evolve, the demand for knowledgeable and licensed professionals remains strong. Whether you are pursuing a career in life, health, property, casualty, or personal lines insurance, obtaining the proper license is an essential first step.

Our courses provide students with the knowledge, resources, and support needed to successfully navigate the licensing process. With flexible learning options, state-specific content, and a commitment to student success, Success CE is proud to help individuals across the nation achieve their professional goals and build rewarding careers in insurance.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

If you are holding an active insurance license in both Life & Health or Property Casualty, you know that meeting CE requirements, on time and correctly, is a non-negotiable part of staying licensed and compliant. That is where Success CE stands out. Here is why many agents use Success CE to renew their Life and Health and Property Casualty licenses:

Nationwide Approval & Wide-Ranging Course Catalog

Success CE’s courses are approved in all 50 states, covering both Life & Health and Property Casualty CE requirements. (Success CE)

Our catalog is not limited to basic CE: we offer courses in ethics, annuities, long-term care, and more allowing you to fulfill specialized requirements specific to your license type or state. (Success CE).

For agents holding licenses in multiple lines (e.g., Life & Health and P&C), this breadth simplifies compliance: you do not need to piece together CE hours from different providers or juggle multiple platforms.

Efficiency – Fast, Easy, and Convenient

We at Success CE emphasizes user convenience: our CE courses are “easy-to-complete,” and they offer same-day real-time reporting of completed credits. (Success CE)

For busy agents who do not want to spend extra time traveling to in-person classes or coordinating schedules especially those balancing Life & Health and P&C CE hours this convenience can save significant time and stress. (Success CE)

Our system allows for both online/self-study CE and live classroom/webinar CE (through a sister service) depending on what your state license renewal requires or which format you prefer. (insurancecontinuingeducation.com)

Cost-Effective – Competitive Pricing and Value

Success CE has a “Guaranteed Lowest Price” for their CE courses. (Success CE)

Given the ability to cover multiple license lines, specialized topics, and potentially bundle CE with other designations or certifications (CFP, CLU/ChFC, etc.), using Success CE may offer good value compared with juggling separate providers for each license line. (Success CE)

Good Reputation & Customer Experience

Customer testimonials highlighted on our site praise the ease of navigation, helpful customer service, and a simple CE process. (Success CE)

Additionally, agents report being able to complete CE quickly and renew licenses without the delays or hassles sometimes associated with other CE providers. (Success CE)

If you have ever had CE renewal frustration (especially juggling multiple license types), working with a provider that emphasizes reliability and service can make a meaningful difference.

Useful for Multi-Line License Holders – One Stop for Everything

Agents licensed in both Life & Health and P&C benefit from a single CE source that supports both license types, simplifying their compliance process.

Because Success CE offers a broad set of CE courses (ethics, annuities, long-term care, etc.), you can meet specialized continuing education requirements (e.g., annuity suitability, ethics) along with general CE hours all in one place. (Success CE)

Therefore, our unified approach reduces administrative overhead and helps ensure you do not miss any required credits for either license type.

Who Benefits Most from Success CE

Agents with multiple licenses (Life & Health and Property & Casualty ) who want to streamline their CE compliance.

Busy professionals who prefer online/self-study CE or flexible scheduling instead of in-person classes.

Agents looking for good value. We offer courses beyond “just the basics,” such as ethics, annuities, or long-term care.

Agencies or firms managing multiple producers Success CE offers services for individual licensees and corporate/agency-level CE administration. (Success CE)

Final Thoughts

For licensed agents juggling multiple license lines; Life & Health Property & Casualty, compliance shouldn’t feel like a chore. Success CE offers one of the most comprehensive, flexible, and cost-effective solutions available today. Their nationwide approvals, broad course catalog, easy-to-use online system, and strong reputation for customer service make them an appealing choice if you want to simplify CE compliance and focus more on serving clients.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

Preparing for a state insurance license or a securities registration exam is one of the most important steps in beginning a new career. Yet for many candidates, the experience can feel overwhelming: dense textbooks, outdated practice questions, and confusing explanations that don’t reflect today’s regulatory landscape.

Our mission is simple: Deliver the most complete, accurate, and user-friendly prelicensing study system available for insurance and securities candidates nationwide.

A Modern Approach to Prelicensing Education

While many providers rely on recycled outlines and decades-old content, PreLicensingTraining reimagined the entire learning process from the ground up. Every chapter, question bank, flashcard, and exam scenario has been built with deliberate intention — focusing on clarity, accuracy, and application.

Below are the core pillars that make our program different.

1. Content Written from the Perspective of Real Instructors

Our materials are not mass-produced or outsourced. They are crafted by experienced instructors who understand both the exam and the industry.

Instead of reading stiff technical paragraphs, students learn through:

Clear explanations

Practical examples

Real-life scenarios

Straightforward definitions

Logical sequencing of topics

This ensures students understand how insurance and securities concepts actually work, not just how to memorize them.

2. Exam-Aligned Structure and Design

Every state’s DOIs and FINRA functions are mapped exactly to the content we create. Our manuals:

Follow the official outlines line-by-line

Include the newest laws, time frames, regulations, and dollar amounts

Break down complicated rules into understandable, usable information

Prepare students for precisely what they will face on the exam

This alignment removes guesswork and increases passing confidence.

3. Professionally-Developed Flashcards

Unlike generic flashcards that simply repeat definitions, ours are designed as true learning tools, featuring:

One core concept per card

Concise questions with direct answers

Coverage of terminology, rules, laws, formulas, and exam-trigger concepts

A structure that reinforces memory retention

Students use them not just to memorize, but to understand.

4. Intelligent Question Banks

Our practice questions are not “randomly generated” or copied from outdated sources. They are written to mirror:

The style of state insurance exams

The structure of FINRA and NASAA tests

The complexity of actual licensing questions

Each question is followed by a clear explanation that teaches why the right answer is correct, and why the wrong answers are not. This builds real test-taking skill rather than encouraging guesswork.

5. Realistic Final Exams

Final exams simulate the look, feel, and pacing of the real test. They include:

Mixed difficulty levels

Scenario-based analysis

Regulatory application questions

Definitions and recall questions

Content-area weighting that matches the real exam

By the time students complete these practice exams, the actual licensing test feels familiar instead of intimidating.

6. Continuous Updating and Accuracy Controls

Regulatory updates happen constantly, both in the insurance industry and the securities world. Success PreLicensing.com maintains a rigorous update process to ensure that curriculum, questions, and examples reflect:

New laws

Revised statutes

Updated licensing requirements

Current regulatory expectations

Clarified exam outlines

Students can trust that what they are learning is relevant today.

Our students consistently report that our materials feel clearer, better organized, and more relevant than anything they’ve used before. They appreciate our:

Straightforward writing

Logical chapter design

Practical examples

Comprehensive coverage

Instructor-built questions

User-friendly structure

Realistic practice exams

Simply put: Our program is built to teach, not confuse.

A Better Way to Prepare for Licensing Exams

Whether your goal is to become an insurance agent, an investment professional, or a dual-licensed producer, Success PreLicensing.com provides a complete and modern preparation system that supports you from start to finish.

We are proud to be part of Success CE, and even more proud to help thousands of students take their first step into the industry with confidence.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

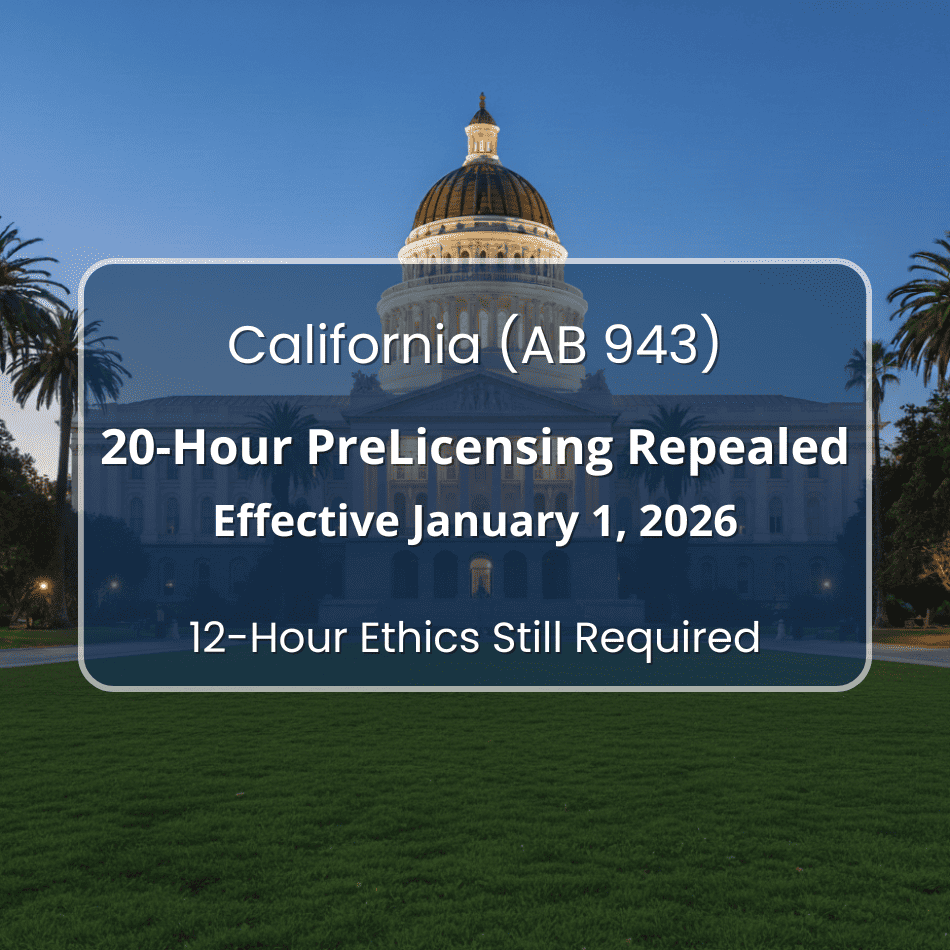

Effective January 1, 2026, CDI will officially eliminate the long-standing California 20-hour prelicensing education requirement for insurance producers.

This major regulatory update, established under AB 943 (Chapter 566, Statutes of 2025), reshapes the path to licensure for new agents across Life, Health, Property, Casualty, Personal Lines, Commercial Lines, and Limited Lines Automobile.

However, one part of the process does not change:

All applicants must still complete the mandatory 12-Hour Ethics & California Insurance Code course and pass the full state licensing exam.

This Ultimate Guide provides the most complete and authoritative breakdown of what is changing, what is staying the same, and how California insurance candidates and agencies should prepare for 2026 and beyond.

1. What AB 943 Means for California Insurance Licensing in 2026

Assembly Bill 943, signed into law on October 10, 2025, updates California Insurance Code §1749 and directly removes the 20-hour line-specific prelicensing education blocks for all major insurance producer licensing types.

Beginning January 1, 2026:

The 20-hour prelicensing requirement is fully repealed.

The 12-Hour Ethics & California Insurance Code requirement remains mandatory.

The state licensing exam continues for every line of authority.

Fingerprinting remains required after exam passage.

Existing 20-hour, 32-hour, and 52-hour courses will be removed from CDI’s public course search on January 1, 2026, and inactivated January 12, 2026.

2. Key Changes at a Glance (Quick Summary for 2026)

Requirement

Status in 2026

Notes

20-Hour Prelicensing

Repealed

Eliminated by AB 943

12-Hour Ethics & California Insurance Code

Required

Must be completed by all producer applicants

State Licensing Exam

Required

Unchanged requirement

Fingerprinting

Required

Must occur after passing the exam

Applies To

Life, A&H, Property, Casualty, Personal Lines, Commercial Lines, Limited Lines Auto

Not Affected

Bail agents; public adjusters

Their 20-hour requirement remains

These changes come directly from CDI’s November 2025 notice and AB 943 implementation guidance.

3. Why California Removed the 20-Hour Prelicensing Requirement

California modernized its licensing pathway to:

Remove barriers to entry for new producers

Streamline the licensing timeline

Prioritize competency through Ethics & Code and exam performance

Align with evolving national standards for producer onboarding

The Legislature determined that the 12-Hour Ethics requirement + the state exam serve as adequate competency benchmarks without the need for additional 20-hour blocks.

4. What the California 20-hour pre-licensing repeal changes on January 1, 2026

A. The California 20-Hour Prelicensing Courses Are No Longer Required

CDI will no longer recognize or display the following course types:

20-Hour line-specific courses

32-Hour (20 + 12 Ethics) blended courses

52-Hour (two lines + Ethics) courses

Life

Accident & Health or Sickness

Property

Casualty

Commercial Lines

Personal Lines

Limited Lines Automobile

These are removed from public catalog on January 1, 2026 and inactivated on January 12, 2026.

Applies to applicants seeking:

Life

Accident & Health or Sickness

Property

Casualty

Commercial Lines

Personal Lines

Limited Lines Automobile

5. What Requirements Stay the Same for California Licensing

A. 12-Hour Ethics & California Insurance Code Requirement

All new resident producer applicants must continue to complete the state-mandated:

12 hours of Ethics and California Insurance Code training (includes the 1-hour antifraud component required since 2023)

B. State Licensing Exam Remains Mandatory

Applicants must still:

Study the official License Examination Objectives

Register with PSI

Pass the exam for each selected line of authority

C. Fingerprinting & Application Sequence

Fingerprinting must be completed after passing the exam, before the license is issued.

D. No Change for Bail Agents or Public Adjusters

Their 20-hour requirement remains fully intact.

6. How to Get Your California Insurance License in 2026 (Step-by-Step)

Beginning January 1, 2026, your licensing process becomes more streamlined. Here is the updated path:

Step 1: Choose your line(s) of authority

Life

Accident & Health or Sickness

Property

Casualty

Personal Lines

Commercial Lines

Limited Lines Auto

Step 2: Complete the 12-Hour Ethics & Code Prelicensing Course

This is now the only educational requirement prior to the exam.

Step 3: Prepare for the State Exam

Use the CDI exam objectives and reputable exam prep solutions.

Step 4: Pass the State Licensing Exam

You must still pass the full exam for each line.

Step 5: Get Fingerprinted & Submit Your Application

Your exam pass is valid only after fingerprint clearance and application submission. These steps come directly from CDI’s 2026 licensing guidance.

7. How the California 20-hour pre-licensing repeal affects Life & Accident & Health

Life & Accident & Health

20-Hour Life and 20-Hour A&H courses repealed

Only 12-Hour Ethics & Code required

Must pass the Life and/or A&H state exam(s)

Property & Casualty

20-Hour Property and 20-Hour Casualty repealed

Combined P&C previously required 40 hours + Ethics; now only Ethics is required

Must pass the P&C exams

Personal Lines, Commercial Lines, and Limited Lines Auto

All 20-hour prelicensing blocks eliminated

Ethics still required

State exam still required

Unaffected License Types

Bail agents

Public insurance adjusters

These continue to require 20 hours of education.

8. 2026 Transition Timeline: What Happens to Old Courses

Through December 31, 2025

Providers may continue delivering all previously approved courses. Rosters must be uploaded within 10 days of completion.

January 1, 2026

CDI removes 20-hour, 32-hour, and 52-hour courses from its online catalog.

January 1-11, 2026

Providers may continue uploading rosters for 2025 completions.

January 12, 2026

CDI officially inactivates all 20/32/52-hour courses. No further roster uploads will be accepted.

9. California 20-hour Prelicensing Requirements: 2025 vs. 2026 Comparison

License Type

Before January 1, 2026

After January 1, 2026

Life

20 Hours + 12 Ethics

12 Ethics only

Accident & Health

20 Hours + 12 Ethics

12 Ethics only

Property

20 Hours + 12 Ethics

12 Ethics only

Casualty

20 Hours + 12 Ethics

12 Ethics only

P&C Combined

40 Hours + 12 Ethics

12 Ethics only

Personal Lines

20 Hours + 12 Ethics

12 Ethics only

Commercial Lines

20 Hours + 12 Ethics

12 Ethics only

Limited Lines Auto

20 Hours + 12 Ethics

12 Ethics only

Bail Agents

20 Hours

20 Hours (unchanged)

Public Adjusters

20 Hours

20 Hours (unchanged)

10. Frequently Asked Questions About the 2026 Prelicensing Changes

1. What happened to California 20-hour prelicensing requirement?

It was repealed under AB 943, effective January 1, 2026.

2. Do I still need prelicensing education in 2026?

Yes. All applicants must complete the 12-Hour Ethics & California Insurance Code course.

3. Do I still need to pass the state exam?

Yes. The exam remains fully mandatory for all lines.

4. What happens to existing 20-hour courses?

They will be removed from CDI’s public course search on January 1, 2026, and officially inactivated on January 12, 2026.

5. Does the repeal affect bail agents or public adjusters?

No. Their 20-hour requirement remains unchanged.

6. Do I still need fingerprinting?

Yes. Fingerprinting is required after exam passage and before licensure.

11. What These Changes Mean for Agencies, Carriers, and Hiring Managers

This regulatory shift impacts hiring pipelines, onboarding workflows, and internal training expectations.

Key impacts:

Faster onboarding for new hires

Reduced friction for prospective producers

More emphasis on exam preparation

Agencies must update internal documentation

Strict Ethics compliance remains essential

Vendors and carriers must update LMS workflows and contracts

The Ethics requirement becomes the single standardized prelicensing education component, placing more weight on selecting a reputable provider.

12. How New Applicants Should Prepare for Licensing in 2026

A. Enroll in the 12-Hour Ethics & Code Course

Since this requirement does not change, completing Ethics early ensures you are exam-ready as soon as the new rules take effect.

B. Begin Exam Preparation

Use resources aligned with CDI’s License Examination Objectives.

C. Monitor CDI updates

CDI may release additional guidance as January approaches.

D. Start the fingerprinting process immediately after passing your exam

13. Final Thoughts and Next Steps for California Insurance Applicants

California’s adoption of AB 943 marks the largest modernization of producer licensing in decades. By removing the 20-hour prelicensing blocks while preserving Ethics education and exam rigor, the state has created a streamlined pathway that benefits both applicants and agencies.

In 2026 and beyond, your required steps are simple:

Complete the 12-Hour Ethics & California Insurance Code course

The insurance industry is no stranger to regulatory change, and 2025 has already brought a wave of updates at both the federal and state level. From healthcare reforms to property and casualty adjustments, regulators are tightening oversight and responding to evolving risks. Below is a summary of the most significant updates—and what they mean for insurance professionals.

Federal Health Insurance and ACA Reforms

The Centers for Medicare & Medicaid Services (CMS) finalized the Marketplace Integrity and Affordability Rule in 2025, introducing several key changes to strengthen oversight of the Affordable Care Act (ACA) marketplaces.

Highlights include:

Stricter Verification: Enhanced income verification and pre-enrollment checks for special enrollment periods (SEPs) to reduce misuse.

Eligibility Adjustments: DACA recipients will no longer qualify as “lawfully present” for marketplace and Basic Health Program eligibility.

Enrollment Windows: Open enrollment will now run from November 1 through December 15 for the 2027 plan year on federal exchanges.

Premium Payment Requirement: Individuals automatically re-enrolled in zero-premium plans will now need to pay a minimum $5 monthly premium.

Tax Credit Reconciliation: Rules around advance premium tax credits (APTCs) have tightened, with consequences for those failing to reconcile past credits.

The Notice of Benefit and Payment Parameters for 2025 introduced consumer-friendly adjustments, aiming to improve plan choice, expand access, and strengthen marketplace standards.

Impact: For insurers and brokers, these changes mean more administrative oversight, stricter compliance, and potential adjustments to plan design and marketing strategies.

State-Level Insurance Developments

California

California has taken the lead with several regulatory shifts:

Auto Insurance: Minimum liability coverage limits doubled in 2025, rising to $30,000 per person / $60,000 per accident for bodily injury, and $15,000 for property damage. These limits will rise again in 2035.

Wildfire and Climate Risk: New rules require insurers to incorporate catastrophe modeling into rate filings and expand coverage options in wildfire-prone areas. Reinsurance cost pass-throughs will also face stricter oversight.

North Carolina

Regulators approved a 5% auto insurance rate increase effective October 1, 2025—far below the much larger hikes initially sought by carriers.

Alabama

A new law allows Alfa Insurance to offer alternative health plans exempt from certain ACA protections. The new law also includes preexisting condition coverage requirements. While promoted as affordable options, critics warn consumers may lose critical safeguards.

Illinois

Illinois is preparing to launch its own state-based health insurance marketplace, moving away from Healthcare.gov beginning in 2026.

Impact: These shifts highlight the growing divergence among states—some expanding protections, others pulling back federal safeguards. Insurers operating across state lines must remain vigilant about varying compliance obligations.

NAIC and Industry-Wide Priorities

The National Association of Insurance Commissioners (NAIC) has laid out its 2025 priorities, reaffirming its commitment to state-based regulation and improved risk oversight. Key initiatives include:

A new Risk-Based Capital (RBC) Model Governance Task Force to review capital standards and better account for catastrophe risk, reinsurance, and market consolidation.

Development of a U.S. version of the Global Insurance Capital Standard, with a draft expected by 2026.

Updated asset adequacy and reinsurance guidelines to improve transparency and strengthen solvency protections.

Impact: These measures signal increasing scrutiny on carriers’ capital adequacy and risk management frameworks. The measures apply to both large insurers and smaller regional players.

What This Means for Insurance Professionals

Taken together, these regulatory updates underscore several key trends:

Compliance is Tightening: Expect more detailed verification, stricter reporting, and less tolerance for administrative errors.

Pricing Pressures Are Rising: Higher liability minimums, climate modeling, and capital requirements will directly impact rate filings and underwriting strategies.

Consumer Access Is Evolving: Some reforms aim to expand choice and affordability, while others could create gaps in coverage—leaving room for brokers and agents to guide clients carefully.

Regulators Are Proactive: Both federal and state regulators are signaling a more hands-on approach to ensuring solvency, sustainability, and fairness.

Final Thoughts

For insurance professionals, the lesson is clear: staying ahead of regulatory change is no longer optional. These new rules will affect everything from product design to client conversations, and the ability to adapt quickly will set successful agents, brokers, and carriers apart.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More