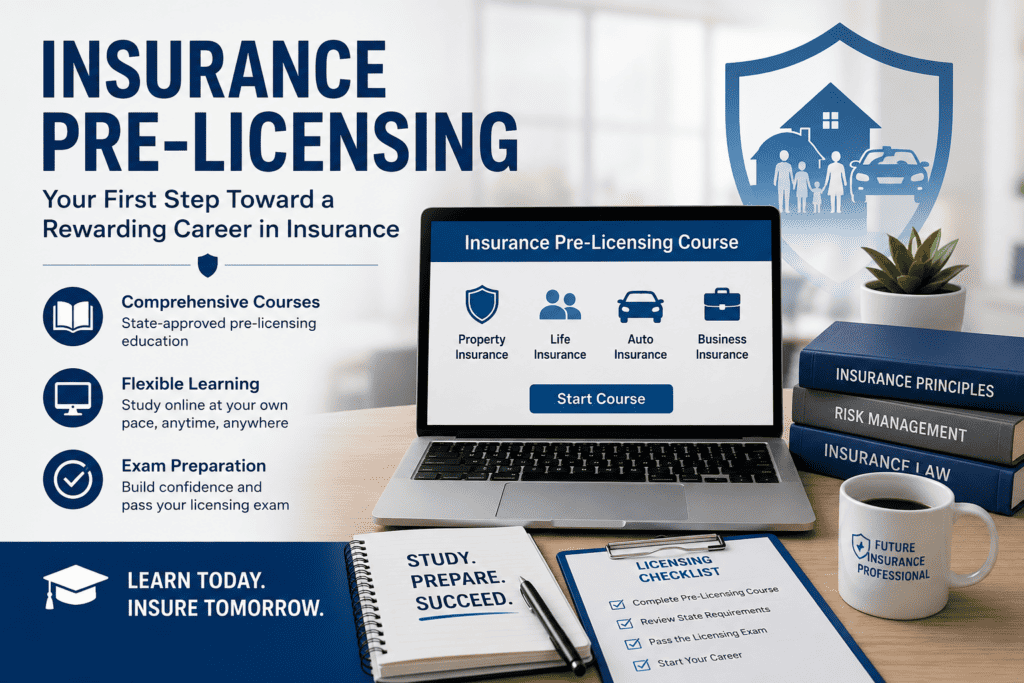

Success CE is pleased to announce that, effective June 1, 2026, our insurance pre-licensing courses are now available in all 50 states effective June 1, 2026

This nationwide expansion allows aspiring insurance professionals across the country to access the training and educational resources needed to prepare for their state licensing examinations and launch successful careers in the insurance industry.

We provide comprehensive, easy-to-understand instruction designed to help students build knowledge, confidence, and exam readiness.

For information regarding available courses, state-specific licensing requirements, and enrollment options, please visit our website or contact our team directly.

As the insurance industry continues to grow and evolve, the demand for knowledgeable and licensed professionals remains strong. Whether you are pursuing a career in life, health, property, casualty, or personal lines insurance, obtaining the proper license is an essential first step.

Our courses provide students with the knowledge, resources, and support needed to successfully navigate the licensing process. With flexible learning options, state-specific content, and a commitment to student success, Success CE is proud to help individuals across the nation achieve their professional goals and build rewarding careers in insurance.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

Preparing for a state insurance license or a securities registration exam is one of the most important steps in beginning a new career. Yet for many candidates, the experience can feel overwhelming: dense textbooks, outdated practice questions, and confusing explanations that don’t reflect today’s regulatory landscape.

Our mission is simple: Deliver the most complete, accurate, and user-friendly prelicensing study system available for insurance and securities candidates nationwide.

A Modern Approach to Prelicensing Education

While many providers rely on recycled outlines and decades-old content, PreLicensingTraining reimagined the entire learning process from the ground up. Every chapter, question bank, flashcard, and exam scenario has been built with deliberate intention — focusing on clarity, accuracy, and application.

Below are the core pillars that make our program different.

1. Content Written from the Perspective of Real Instructors

Our materials are not mass-produced or outsourced. They are crafted by experienced instructors who understand both the exam and the industry.

Instead of reading stiff technical paragraphs, students learn through:

Clear explanations

Practical examples

Real-life scenarios

Straightforward definitions

Logical sequencing of topics

This ensures students understand how insurance and securities concepts actually work, not just how to memorize them.

2. Exam-Aligned Structure and Design

Every state’s DOIs and FINRA functions are mapped exactly to the content we create. Our manuals:

Follow the official outlines line-by-line

Include the newest laws, time frames, regulations, and dollar amounts

Break down complicated rules into understandable, usable information

Prepare students for precisely what they will face on the exam

This alignment removes guesswork and increases passing confidence.

3. Professionally-Developed Flashcards

Unlike generic flashcards that simply repeat definitions, ours are designed as true learning tools, featuring:

One core concept per card

Concise questions with direct answers

Coverage of terminology, rules, laws, formulas, and exam-trigger concepts

A structure that reinforces memory retention

Students use them not just to memorize, but to understand.

4. Intelligent Question Banks

Our practice questions are not “randomly generated” or copied from outdated sources. They are written to mirror:

The style of state insurance exams

The structure of FINRA and NASAA tests

The complexity of actual licensing questions

Each question is followed by a clear explanation that teaches why the right answer is correct, and why the wrong answers are not. This builds real test-taking skill rather than encouraging guesswork.

5. Realistic Final Exams

Final exams simulate the look, feel, and pacing of the real test. They include:

Mixed difficulty levels

Scenario-based analysis

Regulatory application questions

Definitions and recall questions

Content-area weighting that matches the real exam

By the time students complete these practice exams, the actual licensing test feels familiar instead of intimidating.

6. Continuous Updating and Accuracy Controls

Regulatory updates happen constantly, both in the insurance industry and the securities world. Success PreLicensing.com maintains a rigorous update process to ensure that curriculum, questions, and examples reflect:

New laws

Revised statutes

Updated licensing requirements

Current regulatory expectations

Clarified exam outlines

Students can trust that what they are learning is relevant today.

Our students consistently report that our materials feel clearer, better organized, and more relevant than anything they’ve used before. They appreciate our:

Straightforward writing

Logical chapter design

Practical examples

Comprehensive coverage

Instructor-built questions

User-friendly structure

Realistic practice exams

Simply put: Our program is built to teach, not confuse.

A Better Way to Prepare for Licensing Exams

Whether your goal is to become an insurance agent, an investment professional, or a dual-licensed producer, Success PreLicensing.com provides a complete and modern preparation system that supports you from start to finish.

We are proud to be part of Success CE, and even more proud to help thousands of students take their first step into the industry with confidence.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

Summer is often a time for relaxation, vacations, and enjoying the outdoors—but it’s also a great opportunity to help your clients secure their financial futures. While the warmer months can be a slower time for some industries, when it comes to life insurance, summer offers unique opportunities. Whether you’re a seasoned agent or new to the business, here are five tips for selling life insurance in the summer months.

1. Leverage Summer Lifestyle Events

Summer is filled with significant life events that can spark important financial discussions. Weddings, new babies, and graduations are just a few milestones that prompt people to start thinking about their future and family security.

Weddings: Newlyweds are likely thinking about the future, and life insurance can be a key part of their financial planning. Emphasize how life insurance can provide peace of mind for their new life together, especially as they take on new responsibilities.

New Parents: If you know someone who just had a baby, it’s an ideal time to introduce them to life insurance. Parents are often very receptive to the idea of life insurance as a way to ensure their child’s future is secure.

Graduations: Recent grads or parents of graduates might be considering life insurance as part of their financial independence. They may not have thought about it yet, but this is an excellent time to educate them about the benefits of starting early.

2. Host Outdoor or Virtual Community Events

Summer provides the perfect setting for outdoor events or relaxed virtual meetings that help you connect with potential clients. Instead of the traditional office setting, try reaching out in more casual, accessible ways.

Outdoor booths: Set up a booth at a local summer fair, farmer’s market, or community event. People are out and about, enjoying the nice weather and open to talking about their financial goals. It’s a less formal setting where you can engage potential clients in conversations about life insurance.

Virtual info sessions: If in-person events aren’t an option, host virtual webinars or Q&A sessions. Evening webinars work well during summer because people are more likely to be free after work hours. Keep the sessions short and focus on answering common questions to build trust and credibility.

3. Tie Insurance to Seasonal Financial Planning

Many people use the summer to revisit their financial goals. This mid-year review period presents an excellent opportunity to introduce life insurance as part of a larger financial plan.

Mid-year financial checkups: As people evaluate how well they’re doing with their financial goals, use this time to suggest life insurance as a way to strengthen their financial future. Whether it’s securing their family’s well-being or protecting a growing business, life insurance can be a key part of their mid-year financial review.

Tax benefits and cash value growth: Permanent life insurance policies, such as whole life or universal life, come with tax advantages and a cash value component. These types of policies are great for clients looking to grow their wealth while ensuring long-term protection. Highlighting these benefits during the summer when clients are thinking about taxes or savings can boost your sales.

4. Use Summer Themes in Your Marketing

Make your marketing resonate with the season. Summer imagery and language can help you connect with potential clients on an emotional level.

Summer protection themes: Position life insurance as a way to protect what matters most—whether it’s family, health, or financial security. Use summer-related phrases like “Protect your sunny days ahead” or “Secure your family’s future this summer.”

Family-focused messaging: Summer is a time for family vacations, BBQs, and trips to the beach. You can use this imagery to remind clients that life insurance is about creating lasting memories and protecting their loved ones. A family-friendly focus will resonate with parents and grandparents who want to ensure their families are well taken care of.

5. Adjust Your Schedule to Match Clients’ Availability

With the summer months often being a time for vacations and adjusted work schedules, it’s important to be flexible with your availability. People are more likely to be taking time off or working shorter hours, so adjusting your schedule can help you connect with them when it’s convenient.

Offer flexible hours: If your clients are working less in the summer, they might appreciate evening or weekend meetings. Be accommodating to their schedules to make it easier for them to meet with you.

Be available for quick consultations: Sometimes a 10-15 minute phone call or virtual meeting is all it takes to get the conversation started. Offering short, flexible consultations can lead to long-term client relationships.

In Conclusion:

Selling life insurance in the summer may seem challenging at first, but with the right strategies, it can be a lucrative and rewarding time of year. By tapping into summer lifestyle events, adjusting your marketing efforts, and being flexible with your schedule, you can maximize your chances of connecting with potential clients. Whether you’re hosting community events or focusing on financial reviews, remember that life insurance is always relevant—it’s just about making sure you meet your clients when they’re ready to think about the future.

Ready to make this summer your best one yet? Take advantage of these tips, and watch your sales grow!

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

The insurance industry continues evolving in response to market shifts, technological advancements, and consumer demands. In 2024, the sector saw several significant developments that are reshaping its landscape. Here’s a look at the top trends and changes that have impacted the insurance industry this year:

Digital Transformation Accelerated by AI and Automation

Generative AI and Automation: The rise of generative AI in insurance has transformed claims processing, underwriting, and customer service. Automated chatbots powered by AI are handling more inquiries, freeing up human agents for complex issues and creating a smoother experience for customers. Generative AI also supports predictive modeling for underwriting, significantly enhancing efficiency and accuracy.

Claims Management and Fraud Detection: Advanced machine learning models now proactively identify patterns in claims to detect fraud early, saving insurers billions. Automation in claims processing has also led to faster settlements, reducing operational costs and improving customer satisfaction.

Embedded Insurance and Partnerships with Non-Insurance Sectors

New Distribution Channels: Embedded insurance has gained traction as insurers partner with non-insurance industries like e-commerce and travel. Offering coverage directly within these platforms allows insurers to reach customers at their point of need, seamlessly integrating into their purchasing journey. This approach has opened new revenue streams and provided consumers with more accessible coverage options.

Insurtech Collaborations: Insurance companies are increasingly collaborating with insurtech firms to stay competitive. These partnerships enable insurers to adopt innovative technologies quickly, enhancing product offerings and tailoring solutions for various customer segments.

Climate Change and Environmental Risk Management

Climate-Focused Products: As extreme weather events become more frequent and severe, insurers are developing climate-resilient insurance products. Policies that cover flood, wildfire, and hurricane damage are in demand, especially in high-risk areas. Insurers are also incentivizing eco-friendly practices among policyholders, offering discounts for sustainable practices and green infrastructure improvements.

Risk Modeling Innovations: Advanced modeling tools now incorporate climate projections to predict potential losses more accurately. These tools allow insurers to adjust pricing and coverage accordingly, helping them manage risk in an increasingly volatile environment.

Enhanced Regulatory Landscape and Compliance

Privacy and Data Security: With digital transformation comes the challenge of data security. In 2024, regulators emphasized data privacy, and insurers must now comply with stricter data protection laws to safeguard customer information. Compliance with these regulations is essential, as breaches can lead to significant penalties and damage to an insurer’s reputation.

ESG and Sustainability Reporting Requirements: Environmental, Social, and Governance (ESG) metrics are increasingly important for regulators and investors. Many insurers are now required to disclose their ESG practices and sustainability efforts, affecting how they conduct business, manage portfolios, and design products.

Customization through Data Analytics and IoT

Usage-Based Insurance (UBI): Using IoT devices, such as telematics in vehicles, insurers can offer usage-based insurance that tailors coverage and pricing to individual behavior. For example, safer drivers might benefit from lower premiums, while drivers with riskier behaviors pay higher rates. This personalization improves risk assessment accuracy and can lead to greater customer loyalty.

Wearable Tech in Health Insurance: Health insurers are increasingly using wearable devices to track policyholders’ activity levels, promoting preventive healthcare. Policyholders who demonstrate healthier lifestyles can receive premium discounts, creating a win-win situation for insurers and insureds by encouraging wellness and potentially reducing claims.

Focus on Customer-Centric Solutions and Financial Inclusion

Microinsurance and Financial Inclusion: Insurers are broadening their reach by offering microinsurance products to low-income individuals and small businesses. This focus on financial inclusion allows insurers to enter new markets and provide affordable coverage options that protect underserved populations against everyday risks.

Improved Customer Experience: Insurers are prioritizing customer satisfaction by streamlining digital services. Mobile apps, self-service portals, and personalized communication through AI-driven platforms create more engaging and responsive experiences, ultimately increasing customer retention.

Looking Forward

The changes in the insurance industry in 2024 reflect a continued commitment to technology, environmental responsibility, and customer-centered solutions. These developments are likely to persist, pushing the sector toward a future that prioritizes resilience, innovation, and inclusivity. As insurers navigate this new landscape, staying agile and responsive to evolving needs will be key to driving sustainable growth and industry leadership.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

Social security, once a cornerstone of retirement planning in many countries, is undergoing significant transformations in response to demographic shifts, economic pressures, and changing societal expectations. As we stand at the intersection of past promises and future uncertainties, understanding the evolving landscape of social security becomes crucial for individuals, policymakers, and the broader community alike.

A Legacy of Security

Social security systems were originally designed to provide a safety net for retirees, ensuring basic income and healthcare in their later years. For decades, these programs have offered a vital cushion against poverty and hardship among elderly populations. In the United States, for example, Social Security benefits have been a lifeline for millions of retirees since its establishment in the 1930s.

Challenges on the Horizon

However, the landscape is shifting. Several key challenges threaten the sustainability and effectiveness of social security systems worldwide:

Demographic Shifts: Aging populations and declining birth rates in many developed countries mean there are fewer workers contributing to social security systems for every retiree drawing benefits. Therefore, this demographic imbalance strains financial resources and threatens the solvency of these programs.

Economic Pressures: Global economic fluctuations and changing employment patterns influence the financial health of social security funds. Economic recessions, low interest rates, and fluctuations in employment levels impact the contributions and returns on which social security systems rely.

Political and Social Dynamics: Changing political landscapes and societal expectations shape the policies and reforms surrounding retirement. Debates arise about the appropriate age of retirement, the level of benefits, and the balance between public and private provisions.

Adapting to Change

In response to these challenges, countries are exploring various strategies to adapt and ensure the sustainability of their social security systems:

Raising the Retirement Age: Many nations are gradually increasing the age at which individuals become eligible for full benefits. This adjustment aims to align retirement ages with increasing life expectancy and reduce the strain on pension funds.

Enhancing Private Savings: Encouraging individuals to supplement their social security benefits with private savings or pensions is another strategy. Tax incentives, employer-sponsored retirement plans, and financial literacy programs play crucial roles in promoting personal financial preparedness for retirement.

Adjusting Benefit Formulas: Governments may tweak benefit formulas to account for changing economic conditions or demographic realities. These adjustments can include recalculating cost-of-living adjustments or altering the way benefits are calculated based on earnings history.

Investing in Technology: Leveraging technology and data analytics can improve the efficiency of social security administration, reduce fraud, and streamline benefit delivery processes. Digital platforms also enhance accessibility and transparency for beneficiaries.

Looking Ahead

As we peer into the future, the trajectory of retirement remains uncertain yet filled with opportunities for innovation and adaptation. Policymakers, economists, and citizens must collaborate to navigate these changes effectively:

Policy Innovation: Governments must continue to innovate policies that balance fiscal responsibility with the social imperative of providing reliable retirement income.

Public Engagement: Engaging the public in discussions about the future of social security fosters transparency and ensures that reforms reflect the needs and expectations of society.

Global Cooperation: Given the interconnectedness of economies and societies, international cooperation and knowledge-sharing can offer insights into effective retirement practices across borders.

In conclusion, the landscape of social security is evolving in response to demographic shifts, economic pressures, and changing societal expectations. While challenges abound, proactive reforms and innovative strategies can pave the way for sustainable and inclusive social security systems that continue to serve future generations effectively. Embracing change with foresight and collaboration will be essential in shaping a resilient retirement framework for the decades to come.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More