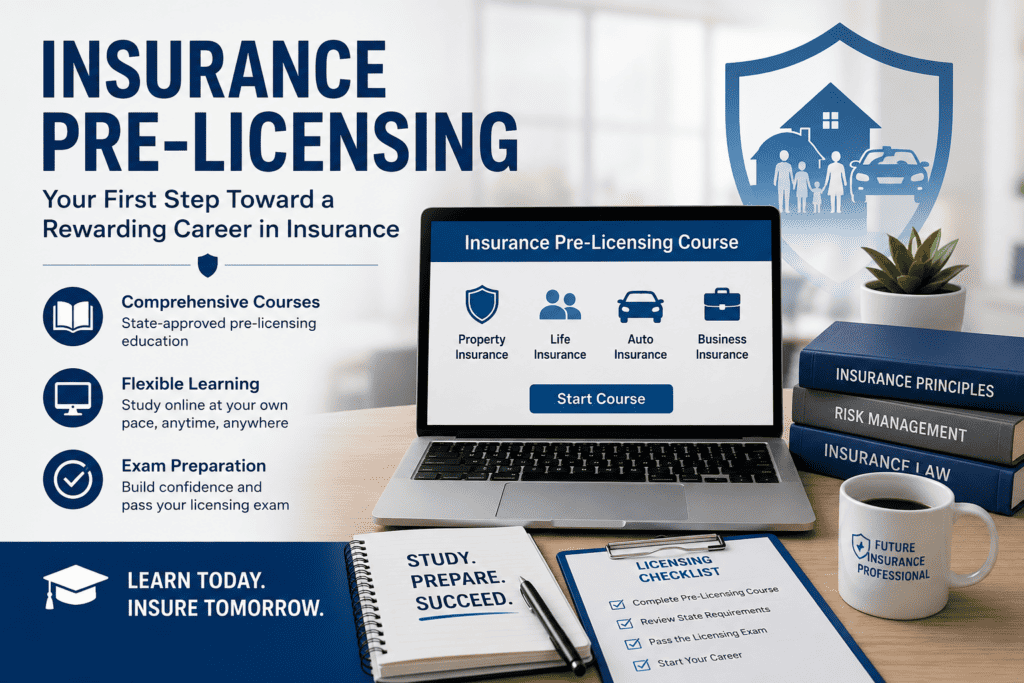

Success CE is pleased to announce that, effective June 1, 2026, our insurance pre-licensing courses are now available in all 50 states effective June 1, 2026

This nationwide expansion allows aspiring insurance professionals across the country to access the training and educational resources needed to prepare for their state licensing examinations and launch successful careers in the insurance industry.

We provide comprehensive, easy-to-understand instruction designed to help students build knowledge, confidence, and exam readiness.

For information regarding available courses, state-specific licensing requirements, and enrollment options, please visit our website or contact our team directly.

As the insurance industry continues to grow and evolve, the demand for knowledgeable and licensed professionals remains strong. Whether you are pursuing a career in life, health, property, casualty, or personal lines insurance, obtaining the proper license is an essential first step.

Our courses provide students with the knowledge, resources, and support needed to successfully navigate the licensing process. With flexible learning options, state-specific content, and a commitment to student success, Success CE is proud to help individuals across the nation achieve their professional goals and build rewarding careers in insurance.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

Preparing for a state insurance license or a securities registration exam is one of the most important steps in beginning a new career. Yet for many candidates, the experience can feel overwhelming: dense textbooks, outdated practice questions, and confusing explanations that don’t reflect today’s regulatory landscape.

Our mission is simple: Deliver the most complete, accurate, and user-friendly prelicensing study system available for insurance and securities candidates nationwide.

A Modern Approach to Prelicensing Education

While many providers rely on recycled outlines and decades-old content, PreLicensingTraining reimagined the entire learning process from the ground up. Every chapter, question bank, flashcard, and exam scenario has been built with deliberate intention — focusing on clarity, accuracy, and application.

Below are the core pillars that make our program different.

1. Content Written from the Perspective of Real Instructors

Our materials are not mass-produced or outsourced. They are crafted by experienced instructors who understand both the exam and the industry.

Instead of reading stiff technical paragraphs, students learn through:

Clear explanations

Practical examples

Real-life scenarios

Straightforward definitions

Logical sequencing of topics

This ensures students understand how insurance and securities concepts actually work, not just how to memorize them.

2. Exam-Aligned Structure and Design

Every state’s DOIs and FINRA functions are mapped exactly to the content we create. Our manuals:

Follow the official outlines line-by-line

Include the newest laws, time frames, regulations, and dollar amounts

Break down complicated rules into understandable, usable information

Prepare students for precisely what they will face on the exam

This alignment removes guesswork and increases passing confidence.

3. Professionally-Developed Flashcards

Unlike generic flashcards that simply repeat definitions, ours are designed as true learning tools, featuring:

One core concept per card

Concise questions with direct answers

Coverage of terminology, rules, laws, formulas, and exam-trigger concepts

A structure that reinforces memory retention

Students use them not just to memorize, but to understand.

4. Intelligent Question Banks

Our practice questions are not “randomly generated” or copied from outdated sources. They are written to mirror:

The style of state insurance exams

The structure of FINRA and NASAA tests

The complexity of actual licensing questions

Each question is followed by a clear explanation that teaches why the right answer is correct, and why the wrong answers are not. This builds real test-taking skill rather than encouraging guesswork.

5. Realistic Final Exams

Final exams simulate the look, feel, and pacing of the real test. They include:

Mixed difficulty levels

Scenario-based analysis

Regulatory application questions

Definitions and recall questions

Content-area weighting that matches the real exam

By the time students complete these practice exams, the actual licensing test feels familiar instead of intimidating.

6. Continuous Updating and Accuracy Controls

Regulatory updates happen constantly, both in the insurance industry and the securities world. Success PreLicensing.com maintains a rigorous update process to ensure that curriculum, questions, and examples reflect:

New laws

Revised statutes

Updated licensing requirements

Current regulatory expectations

Clarified exam outlines

Students can trust that what they are learning is relevant today.

Our students consistently report that our materials feel clearer, better organized, and more relevant than anything they’ve used before. They appreciate our:

Straightforward writing

Logical chapter design

Practical examples

Comprehensive coverage

Instructor-built questions

User-friendly structure

Realistic practice exams

Simply put: Our program is built to teach, not confuse.

A Better Way to Prepare for Licensing Exams

Whether your goal is to become an insurance agent, an investment professional, or a dual-licensed producer, Success PreLicensing.com provides a complete and modern preparation system that supports you from start to finish.

We are proud to be part of Success CE, and even more proud to help thousands of students take their first step into the industry with confidence.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

The insurance industry is no stranger to regulatory change, and 2025 has already brought a wave of updates at both the federal and state level. From healthcare reforms to property and casualty adjustments, regulators are tightening oversight and responding to evolving risks. Below is a summary of the most significant updates—and what they mean for insurance professionals.

Federal Health Insurance and ACA Reforms

The Centers for Medicare & Medicaid Services (CMS) finalized the Marketplace Integrity and Affordability Rule in 2025, introducing several key changes to strengthen oversight of the Affordable Care Act (ACA) marketplaces.

Highlights include:

Stricter Verification: Enhanced income verification and pre-enrollment checks for special enrollment periods (SEPs) to reduce misuse.

Eligibility Adjustments: DACA recipients will no longer qualify as “lawfully present” for marketplace and Basic Health Program eligibility.

Enrollment Windows: Open enrollment will now run from November 1 through December 15 for the 2027 plan year on federal exchanges.

Premium Payment Requirement: Individuals automatically re-enrolled in zero-premium plans will now need to pay a minimum $5 monthly premium.

Tax Credit Reconciliation: Rules around advance premium tax credits (APTCs) have tightened, with consequences for those failing to reconcile past credits.

The Notice of Benefit and Payment Parameters for 2025 introduced consumer-friendly adjustments, aiming to improve plan choice, expand access, and strengthen marketplace standards.

Impact: For insurers and brokers, these changes mean more administrative oversight, stricter compliance, and potential adjustments to plan design and marketing strategies.

State-Level Insurance Developments

California

California has taken the lead with several regulatory shifts:

Auto Insurance: Minimum liability coverage limits doubled in 2025, rising to $30,000 per person / $60,000 per accident for bodily injury, and $15,000 for property damage. These limits will rise again in 2035.

Wildfire and Climate Risk: New rules require insurers to incorporate catastrophe modeling into rate filings and expand coverage options in wildfire-prone areas. Reinsurance cost pass-throughs will also face stricter oversight.

North Carolina

Regulators approved a 5% auto insurance rate increase effective October 1, 2025—far below the much larger hikes initially sought by carriers.

Alabama

A new law allows Alfa Insurance to offer alternative health plans exempt from certain ACA protections. The new law also includes preexisting condition coverage requirements. While promoted as affordable options, critics warn consumers may lose critical safeguards.

Illinois

Illinois is preparing to launch its own state-based health insurance marketplace, moving away from Healthcare.gov beginning in 2026.

Impact: These shifts highlight the growing divergence among states—some expanding protections, others pulling back federal safeguards. Insurers operating across state lines must remain vigilant about varying compliance obligations.

NAIC and Industry-Wide Priorities

The National Association of Insurance Commissioners (NAIC) has laid out its 2025 priorities, reaffirming its commitment to state-based regulation and improved risk oversight. Key initiatives include:

A new Risk-Based Capital (RBC) Model Governance Task Force to review capital standards and better account for catastrophe risk, reinsurance, and market consolidation.

Development of a U.S. version of the Global Insurance Capital Standard, with a draft expected by 2026.

Updated asset adequacy and reinsurance guidelines to improve transparency and strengthen solvency protections.

Impact: These measures signal increasing scrutiny on carriers’ capital adequacy and risk management frameworks. The measures apply to both large insurers and smaller regional players.

What This Means for Insurance Professionals

Taken together, these regulatory updates underscore several key trends:

Compliance is Tightening: Expect more detailed verification, stricter reporting, and less tolerance for administrative errors.

Pricing Pressures Are Rising: Higher liability minimums, climate modeling, and capital requirements will directly impact rate filings and underwriting strategies.

Consumer Access Is Evolving: Some reforms aim to expand choice and affordability, while others could create gaps in coverage—leaving room for brokers and agents to guide clients carefully.

Regulators Are Proactive: Both federal and state regulators are signaling a more hands-on approach to ensuring solvency, sustainability, and fairness.

Final Thoughts

For insurance professionals, the lesson is clear: staying ahead of regulatory change is no longer optional. These new rules will affect everything from product design to client conversations, and the ability to adapt quickly will set successful agents, brokers, and carriers apart.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

The California Department of Insurance (CDI) has introduced a new 8-hour annuity training requirement aimed at enhancing consumer protection and ensuring insurance professionals are well-versed in the intricacies of annuity products. California’s new 8-Hour Annuity Training updates the state’s commitment to equipping insurance agents with the knowledge necessary to offer suitable recommendations and maintain transparency.

Here’s what insurance professionals need to know about this important update.

Annuities are complex financial products that serve as an essential tool for retirement planning. However, their intricacies often make it challenging for consumers to fully understand their benefits, costs, and risks. CDI’s updated training standard aligns with the National Association of Insurance Commissioners (NAIC) Model Regulation #275, which seeks to ensure that consumers receive clear and informed guidance.

This change is designed to:

Protect consumers by improving the quality of recommendations.

Ensure compliance with California’s best interest standards.

Provide agents with comprehensive knowledge of annuity types, benefits, and risks.

The Key Requirements

Initial Training for New Agents All newly licensed agents who intend to sell annuity products in California must complete 8 hours of training before offering or soliciting annuities. This foundational course covers critical topics, including:

Types and classifications of annuities.

Suitability and best interest standards.

Tax implications and benefits of annuities.

How to address potential consumer concerns.

Ongoing Training for Existing Agents Agents who have already completed their initial annuity training must complete a 4-hour refresher course every two years to stay current on regulatory updates and emerging trends.

Focus on Best Interest Standards A significant portion of the training focuses on the best interest obligations outlined in recent regulations. Agents are required to prioritize consumer needs over their own compensation and ensure recommendations align with the client’s financial goals.

How This Impacts Insurance Professionals

The new requirements might feel like an additional step, but they offer long-term benefits:

Enhanced Credibility: Comprehensive training builds trust with clients, as it ensures agents can clearly explain the nuances of annuity products.

Compliance Assurance: Staying updated with regulatory standards minimizes the risk of legal and financial penalties.

Competitive Advantage: Agents who demonstrate a deeper understanding of annuity products are more likely to gain a competitive edge in the marketplace.

Conclusion

The new 8-hour annuity training requirement reflects California’s dedication to protecting consumers while ensuring agents are well-equipped to navigate the complexities of annuity sales. While it may require additional time and effort, this update is an opportunity for insurance professionals to enhance their skills, build trust with clients, and ensure compliance in a competitive industry.

By embracing these changes proactively, agents can not only meet regulatory obligations but also position themselves as knowledgeable and trustworthy advisors in the evolving insurance landscape.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More

In an effort to bolster integrity within the insurance industry, California has introduced a new continuing education (CE) requirement focused on fraud prevention and awareness. Starting in 2024, all licensed insurance professionals in California must complete a dedicated course on insurance fraud as part of their license renewal process. This requirement comes at a time when the state aims to curb rising fraudulent activities and educate industry members on identifying, reporting, and preventing fraudulent schemes.

Here’s an overview of what the new requirement entails, why it’s important, and how it affects insurance professionals in California.

What Is the New Requirement?

As part of California’s ongoing commitment to consumer protection, the Department of Insurance now mandates that insurance agents and brokers complete a one-hour CE course on insurance fraud. This is a new addition to the existing CE requirements for all lines of insurance. The course must be completed as part of the license renewal process and is specifically designed to equip professionals with knowledge and tools to recognize fraud and understand their legal obligations.

Why Is This Requirement Important?

Fraud in the insurance industry is a costly problem. It affects policyholders through higher premiums, reduces trust in the industry, and impacts insurers’ financial stability. According to the California Department of Insurance, insurance fraud costs billions of dollars each year. By introducing this requirement, the state seeks to reduce the impact of fraud by:

Raising Awareness: Educating insurance professionals on common fraud schemes in areas such as workers’ compensation, auto insurance, life insurance, and healthcare.

Encouraging Reporting: Providing guidance on how to report suspected fraud and the protections in place for those who report it.

Supporting Compliance: Ensuring that agents and brokers understand the legal and ethical standards required to identify and prevent fraud.

Who Is Required to Complete This Course?

The new fraud-focused CE requirement applies to all licensed insurance professionals in California. Whether working in life and health, property and casualty, or any other line, licensees must complete this course to meet their renewal obligations. This requirement is for both resident and non-resident licensees, ensuring a consistent standard of fraud education across the board.

Key Topics Covered in the Fraud CE Course

The required fraud course will cover several essential topics aimed at broadening professionals’ understanding of fraudulent practices, including:

Common Fraud Schemes: Educating agents on typical fraud tactics used by policyholders, providers, or even internal employees.

Red Flags and Warning Signs: Learning the indicators of fraud and how to detect suspicious claims and transactions.

Reporting Requirements: Understanding the mandatory reporting rules for suspected fraud and the processes for submitting reports.

Legal and Ethical Obligations: Reinforcing ethical standards and legal responsibilities to maintain compliance and avoid potential penalties.

Case Studies: Reviewing real-world examples to help illustrate fraud tactics and successful prevention measures.

Compliance and Penalties

Insurance professionals who fail to complete this course risk having their license renewal applications denied. Ensuring compliance with the fraud CE requirement not only keeps licenses in good standing but also supports the broader goals of protecting consumers and maintaining a healthy, trustworthy insurance environment.

Practical Tips for Meeting the New Requirement

For agents and brokers preparing for their next renewal cycle, here are some tips for easily incorporating the new fraud requirement:

Plan Ahead: Avoid last-minute cramming by adding the one-hour fraud course to your CE schedule early in your renewal cycle.

Choose Accredited Providers: Select courses from approved CE providers to ensure you meet the state’s standards and receive credit.

Apply What You Learn: Use the knowledge from the course to proactively address potential fraud cases in your day-to-day work.

Stay Informed: Fraud schemes constantly evolve, so stay current with the latest trends and best practices beyond just this course.

Conclusion

The introduction of a mandatory fraud awareness course in California underscores the state’s dedication to tackling insurance fraud. By fostering a more fraud-aware insurance workforce, this requirement not only benefits professionals but also serves as an important measure to protect consumers and support a stable insurance marketplace. As an insurance professional in California, taking this new requirement seriously and applying the learnings in your practice will help build a stronger, more secure industry for all.

This new CE mandate is a step forward for both individual professionals and the industry at large. Embracing it not only fulfills regulatory obligations but also strengthens the overall credibility and resilience of California’s insurance sector.

Why Use Success CE

The Success Family of Continuing Education Companies provides the highest quality Life/Health and Property/Casualty Insurance Continuing Education. CFP Continuing Education, CIMA Continuing Education, CPA Continuing Education, CLU/ChFC (PACE) Continuing Education, and MCLE (Legal). Continuing Education available in all 50 states in Live Insurance, Online Insurance, and Textbook Insurance formats. Learn More